CCW Insurance Doesn’t Cover What You Think It Covers

Written By

Michael Crites

Licensed Concealed Carry Holder

Reviewed by

Editorial Team

Learn About The Editorial Team

Share:

Products are selected by our editors. We may earn a commission on purchases from a link. How we select gear.

Updated

Apr 2026

Sometime around 2011, depending on who you ask, the phrase “CCW insurance” entered the carry conversation as shorthand for a new product category. The permit system had expanded fast enough after Heller that the legal exposure of a lawful defensive use had become a real market, and companies were moving to fill it.

The reasoning behind the category is genuinely sound. Defensive gun uses generate legal costs regardless of outcome — a grand jury investigation alone can run $20,000 to $50,000 in attorney fees before a shot is fired in a courtroom, and a serious criminal trial can reach well into the high six figures. Most carriers can’t self-fund that exposure. Get a plan, know you’re covered.

That last part is where it gets complicated.

In This Article

What the Advice Gets Right and What It Misses

The conventional wisdom in CCW communities has settled on a simple formulation: pick one of the major plans, pay your dues, and cross “legal protection” off the list. USCCA, CCW Safe, and US LawShield are the three dominant options. The marketing for all three runs along the same lines — protection, coverage, “we’ve got your back.” Read the actual documents and a different picture emerges. These are not structurally similar products at different price points. They are three different legal instruments that happen to use the same marketing vocabulary.

This matters most to the carrier who has already made the decision. Not someone who hasn’t gotten around to it — the experienced carrier who wrote the check, filed the card in the wallet, and considers the question settled.

What the Documents Actually Say

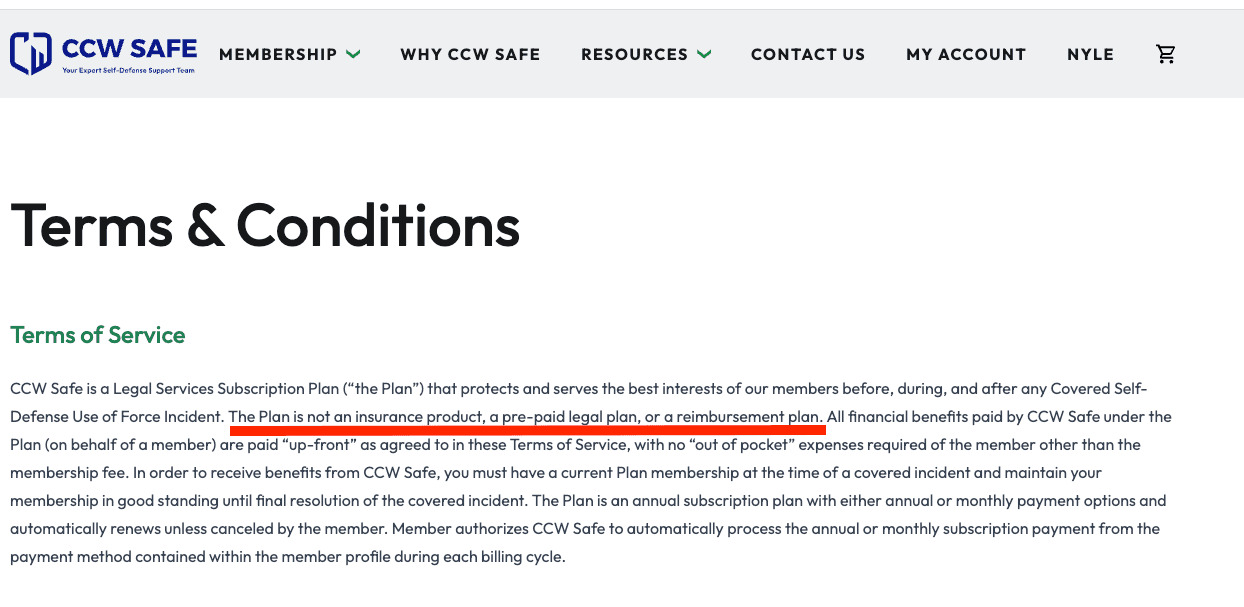

Start with CCW Safe. Their Terms of Service — updated September 20, 2024 — open with this in the first paragraph: “The Plan is not an insurance product, a pre-paid legal plan, or a reimbursement plan.” This isn’t buried language. CCW Safe is stating, before any coverage details appear, that you did not buy insurance.

The practical consequence follows directly: CCW Safe operates outside state insurance regulatory frameworks. If they dispute coverage for your incident, you are not filing a complaint with your state insurance commissioner. You are going to binding arbitration in Oklahoma City, under Oklahoma law, administered by the American Arbitration Association. That clause is also in the Terms.

Whether CCW Safe’s approach is better or worse than regulated insurance is a legitimate question, and in some respects the answer favors CCW Safe. Their payment model is upfront — no out-of-pocket costs while your case is active, no reimbursement after acquittal — and they carry no fixed cap on criminal defense attorney fees, which is a real structural advantage over plans that do.

But a service contract and an insurance policy are different instruments with different regulatory protections, and most carriers who buy CCW Safe believe they bought insurance. They didn’t.

USCCA is structured differently, and the structure matters. Members are not the named insured on USCCA’s policy. The named insured is United States Concealed Carry Association, Inc. Members are additional insureds on a Self-Defense Liability Coverage policy issued to USCCA by Universal Fire and Casualty Insurance Company — policy form SDL 00 02 10 25 if you want to look it up.

This is real insurance, and that distinction from CCW Safe’s service contract is meaningful. But it introduces its own complication: the entity that decides whether your incident qualifies as self-defense is not USCCA. It is Universal Fire and Casualty.

The policy’s exclusion language covers “Criminal Acts for Which Self-Defense is Inapplicable” — meaning no coverage for incidents where self-defense is not available as a legal justification under applicable law. The insurer makes this determination. If Universal Fire and Casualty’s assessment of your incident differs from yours, that’s where the coverage dispute begins.

Not at an insurance commission, but in the policy language — and the gap between those two positions is the gap where the gap where cases like Giles v. Delta Defense LLC (W.D. La., 2019) originate.

Giles, a USCCA Platinum member, received $50,000 of her authorized $150,000 criminal defense coverage after a 2018 shooting, then had coverage cut off before trial. She sued; the case was dismissed in 2022 after her murder conviction. The insurer’s coverage determination came before the jury’s.

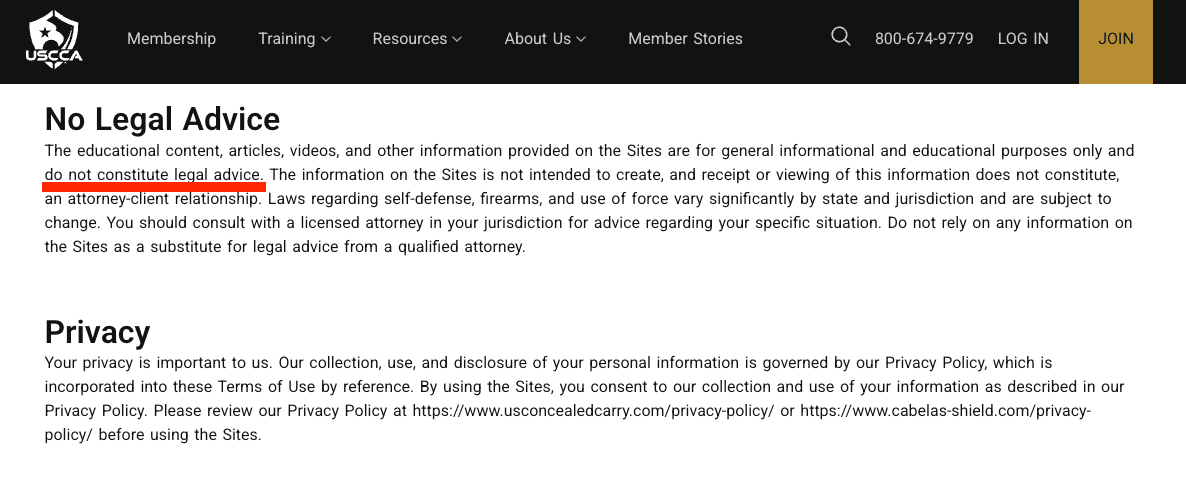

The USCCA membership agreement contains one more piece of language worth noting. In bolded text, it disclaims that informational statements on the USCCA website “do not constitute professional advice” and that USCCA “does not provide any warranty as to their accuracy.” The website that sold you the membership is explicitly disclaimed by the document that governs it.

The US LawShield Oregon “Defend” policy — underwritten by Lyndon Southern Insurance Company under form LDSD.DEF OR 1024 — is real insurance. It is also the starkest example of the gap between what a plan’s name implies and what its document delivers. Section VII(A) is titled “Coverage Eligibility Limited to Residence.”

The text is direct: incidents must have occurred within the Residence. Section IV(C) defines Residence as the primary home or dwelling unit. The policy explicitly excludes all legal services and benefits for any incident occurring “at, in, or on any location other than the Residence.”

An Oregon carry permit holder who purchases US LawShield’s Defend product believing they have coverage for incidents that occur while carrying does not have that coverage. Not reduced coverage. No coverage.

One limitation to state plainly: this analysis is based on the Oregon-specific document and pertains to their “The Defend Plan” designed for those who don’t carry firearms outside the home. Their “Discover, Explore, and Navigate Plans” do cover OOH carry situations.

What the Oregon document suggests, however, is that a home defense insurance product and a carry coverage product can share a distribution channel and a marketing context without sharing coverage terms. Verify your state’s version and select your product carefully.

What to Actually Check

Before the next renewal, four questions are worth answering from the document itself, not the plan’s website.

- First: is your plan actual insurance regulated by a state insurance commissioner, or an unregulated service contract?

- Second: are you the named insured, or an additional insured — and if additional, who controls coverage decisions?

- Third: does your plan cover incidents outside your home?

- Fourth: what is the coverage trigger, and who decides whether your incident meets it?

None of this is an argument for canceling coverage. Pre-purchasing legal defense capacity is sound risk management, and a plan with structural limitations is considerably better than a six-figure attorney bill funded by home equity.

The point is the difference between “I have coverage” and “I understand what I have coverage for.” Only one of those is worth carrying.

The Objection Worth Taking Seriously

The straightforward objection is that all of this is disclosed. The terms are accessible, the policy documents exist, and buyers who didn’t read them made that choice. This is correct, and I’m not disputing it. The argument is narrower: the gap between consumer-facing marketing and policy-level language is structural, not incidental.

When USCCA’s own membership agreement contains a bolded warranty disclaimer for its marketing copy, the gap was designed into the product. The disclosure is real. The expectation the marketing creates is also real. Both are true simultaneously.

The second objection: most defensive gun uses are clear enough that structural nuances don’t govern outcomes. Also correct. The nuances become most consequential in exactly the cases where coverage is most needed — the ambiguous incident, the prolonged investigation, the civil suit that arrives eighteen months after the criminal case closes.

The carrier in the clear-cut case probably doesn’t need the fine print. The carrier in the complicated case does.

The Part That's Actually Eight Pages

You own a defensive pistol and you probably know its specs from memory: trigger pull weight, magazine capacity, which defensive load it runs most reliably. The document that governs whether you have legal defense coverage — and under what conditions — is eight to fourteen pages depending on the plan. It’s available on the plan’s website, and it uses plain enough language that a careful read takes about thirty minutes.

That’s a reasonable investment given what you’re carrying it for.

Sign up for our newsletter

Get discounts from top brands and our latest reviews!